Key takeaways

- 20% of consumers abandon purchases when their preferred payment method isn't available, which hurts conversion for international expansion.

- Payment preferences vary drastically by region: cards represent 57% of US transactions but just 16% in Germany, where 77% of users prefer PayPal.

- Local payment methods include digital wallets (PayPal, Alipay, GCash), bank transfers (iDEAL, SEPA), BNPL services, mobile money, and regional card networks.

- Paddle data shows that enabling local payment methods increases checkout conversion from 4.3 to 6.5 percentage points—a 51% improvement in conversion rates.

- Traditional payment providers require separate integrations per method; Paddle offers 30+ payment methods with zero development work and automatic updates via smart routing.

Your product works perfectly in ten countries, but your checkout only converts well in three. Your app has users across Southeast Asia, but half of them can't complete a purchase because you only accept cards. The gap between where you can deliver value and where you can collect revenue often comes down to a simple mismatch: the payment methods you offer don't align with how people want to pay.

What are local payment methods?

Local payment methods are region-specific ways people prefer to pay for goods and services.

While credit and debit card payment dominates in markets like the US and UK, many regions rely heavily on alternatives. In the Netherlands, iDEAL processes 70% of online transactions. Brazil's customers prefer boleto bancário for online purchases, and China's market runs on Alipay and WeChat Pay.

Types of local payment methods

Understanding the landscape helps clarify why a card-only checkout limits your reach.

Local payment methods fall into several categories, each serving different user needs and regional infrastructures.

Digital wallets store payment credentials and enable quick checkout without entering card details each time. PayPal dominates in Western markets, particularly Germany where it processes 77% of transactions. In Asia, Alipay and WeChat Pay are essential for the Chinese market, while GCash leads in the Philippines, and GrabPay serves Southeast Asia broadly. These wallets often extend beyond payments into everyday apps, making them the natural payment choice.

Bank transfers and direct debits let customers pay directly from their bank accounts, typically with lower fees than cards. iDEAL is the standard in the Netherlands. SEPA direct debit serves the eurozone for recurring payments. Przelewy24 dominates Poland. These methods appeal to users who prefer not to use credit cards or want to avoid card fees.

Buy now, pay later (BNPL) services split purchases into installments, increasing purchasing power without requiring credit cards. Klarna operates across Europe and the US. In the Middle East, Tabby and Tamara cater to markets where Sharia-compliant payment options matter. BNPL has become particularly important for SaaS companies with higher-priced annual plans and app developers with premium tier offerings.

Mobile money and cash-based methods serve markets with lower banking penetration. In parts of Africa and Asia, mobile money accounts let users pay via SMS on feature phones, growing 12% annually. Brazil's boleto bancário generates a voucher customers can pay at physical locations. These methods open markets that cards simply can't reach.

Regional card networks operate alongside global schemes like Visa and Mastercard. France's Cartes Bancaires has over 71 million cards in circulation. Saudi Arabia's Mada serves the domestic market. While these are technically cards, they require specific integrations separate from standard card processing.

Popular payment options by region

The payment methods you need depend entirely on where your customers are. What converts in one market can be completely irrelevant in another.

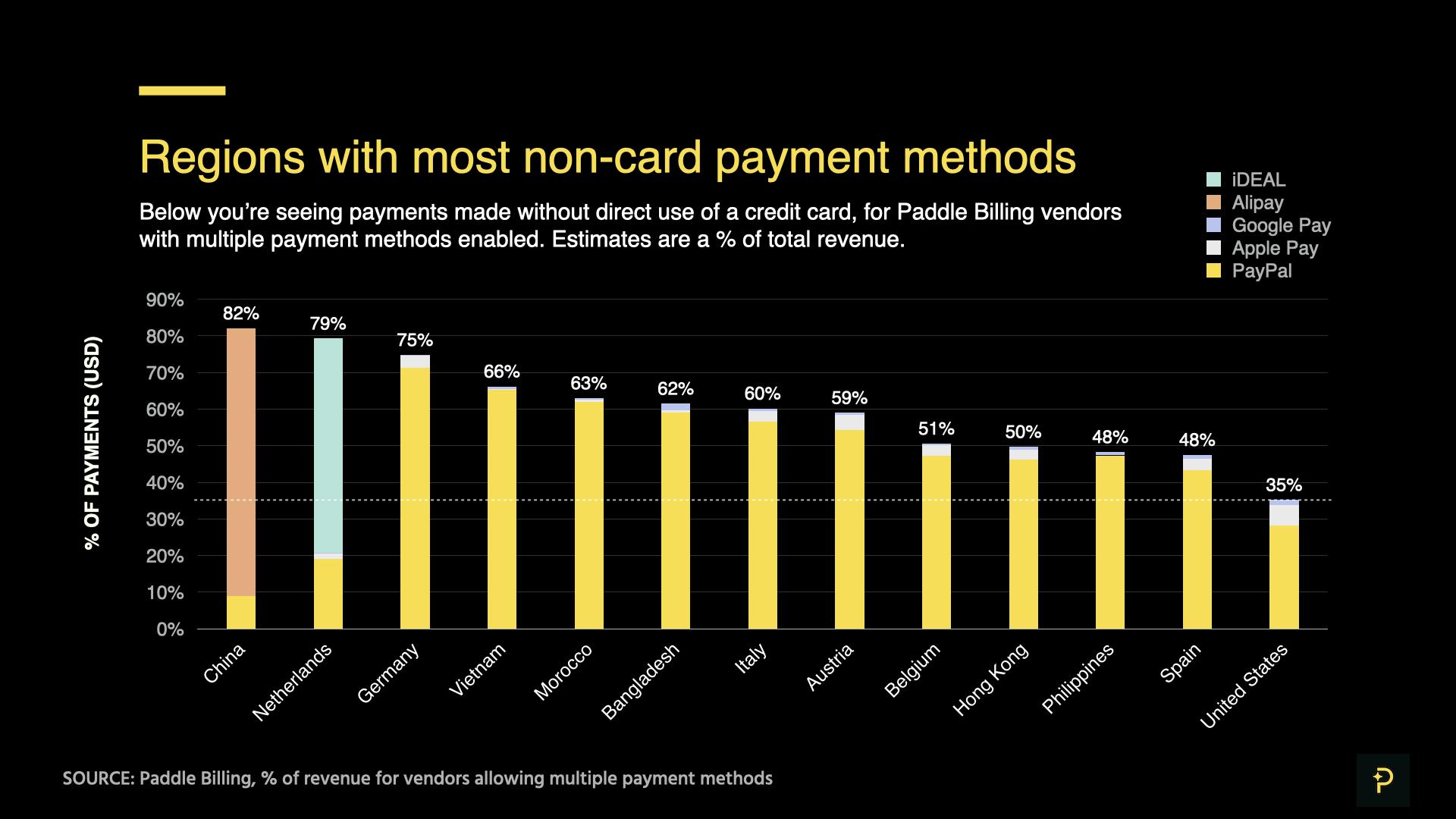

Paddle data shows dramatic differences in non-card payment preferences across regions. The percentages below represent the share of total revenue coming from non-card payment methods - higher percentages indicate markets where cards play a smaller role and local payment methods become essential.

Europe

- Germany (73% non-card revenue): PayPal dominates, followed by Google Pay and Apple Pay. Cards account for less than 30% of transactions

- Netherlands (73% non-card revenue): iDEAL is the primary payment method, with PayPal as secondary option

- Switzerland (62% non-card revenue): Mix of PayPal, Apple Pay, and Google Pay

- Austria (59% non-card revenue): PayPal leads, with wallet methods growing

- Denmark (54% non-card revenue): PayPal and digital wallets preferred over cards

- Belgium: Bancontact for one-time purchases

- Poland: BLIK for one-time purchases

- Portugal: MB WAY for one-time purchases

- France: Cartes Bancaires card network alongside standard cards

Asia-Pacific

- China (82% non-card revenue): Alipay is essential—cards rarely used for online transactions

- Malaysia (66% non-card revenue): PayPal and digital wallets dominate

- Hong Kong (50% non-card revenue): Mix of Alipay, PayPal, and card payments

- Philippines (48% non-card revenue): Growing preference for digital wallets and PayPal

- South Korea: 22+ local card networks (Shinhan, Hyundai, Samsung, Kookmin), plus Naver Pay and Kakao Pay

- India: UPI International available in early access

- Singapore, Australia, Japan: Cards remain primary, but PayPal, Apple Pay, and Google Pay growing

Latin America

- Brazil (44% non-card revenue): Pix available in early access for one-time payments

- Mexico (63% non-card revenue): PayPal leads non-card methods

- Region-wide: Bank transfers and digital wallets increasingly preferred over cards

Middle East

- UAE (60% non-card revenue): PayPal and wallet methods growing, though cards still common

- Saudi Arabia: Local card networks and digital payment preferences

North America

- United States (16% non-card revenue): Cards still dominate, but PayPal, Apple Pay, and Google Pay make up significant share of transactions

- Canada: Similar to US with cards primary, wallets growing

Knowing the dominant local payment method matters most when expanding beyond your initial market. An app succeeding in the US app store will hit friction when launching web subscriptions in Germany without PayPal or SEPA. An app with traction in Southeast Asia needs GrabPay and regional wallets to convert mobile web users effectively.

Why offering local payment methods matters for growth

When you don't offer someone's preferred payment method, they leave. For a SaaS company trying to expand into DACH or an app developer launching in Southeast Asia, that's not acceptable attrition.

Payment preferences reflect deeper market dynamics. In Germany, low credit card penetration means bank transfers and PayPal dominate. Digital wallets lead in many Asian markets because they're tied to everyday apps people already use. In Latin America, cash-based options remain popular because many users lack traditional banking access.

When app developers expand beyond the app store to web-based subscriptions, you're competing with both app store convenience and local payment expectations. Someone who happily pays through Apple Pay in your iOS app might expect iDEAL when they hit your web checkout in Amsterdam. Someone accessing your app through a mobile browser in Manila might prefer GCash over entering card details on a small screen.

The complexity trap

Adding local payment methods sounds simple until you actually try to do it. Each payment method comes with its own integration requirements, API specifications, and authentication flows. SEPA direct debit works differently from ACH. WeChat Pay has different requirements than PayPal. Buy now, pay later services each have their own onboarding process.

Then there's maintenance when APIs update, regulations change, or new security requirements emerge. If you're managing these integrations yourself, someone on your team needs to stay on top of every update across every method you support.

The compliance burden multiplies with each market you enter. Tax rules vary by country. Some payment methods require specific legal agreements, and others have regional licensing requirements. If you're using a traditional payment provider, you're typically the merchant of record, which means you're responsible for all of this.

Many companies respond by avoiding certain markets entirely. App developers stick with the app stores, accepting the 30% commission rather than dealing with payment complexity. Both approaches leave money on the table.

How Paddle eliminates the development burden

As a merchant of record, Paddle handles payment infrastructure so you don't have to. The platform offers 30+ local payment methods, and you never integrate or maintain them yourself. When Paddle adds a new payment method or updates an existing one, it appears in your checkout automatically.

Smart payment routing automatically determines which payment methods to show each customer based on location, transaction amount, and currency. A customer in Berlin sees different options than someone in Singapore.

The numbers show the impact. Enabling local payment methods increases checkout conversion from 4.3 percentage points without local payment methods to 6.5 percentage points with them. That's a 51% improvement simply from offering local payment methods people want to use.

When privacy platform AdGuard needed to expand into China, their previous payment provider didn't support Alipay, so they couldn't effectively serve their growing user base there. They also needed seamless PayPal integration, which typically requires separate contracts and negotiations. With Paddle, both payment methods were immediately available with zero development work. Read how AdGuard scaled to 150 million users globally without building a payments team.